From the Editor - September 2013 by Michael Forlenza

|

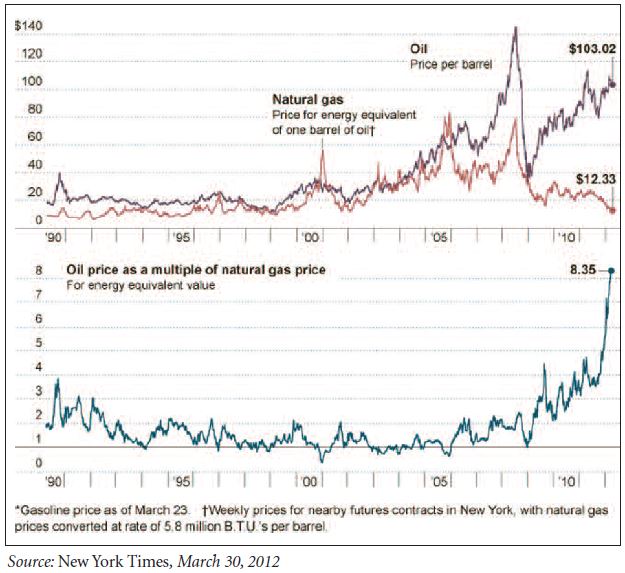

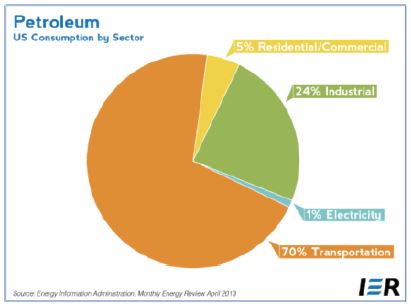

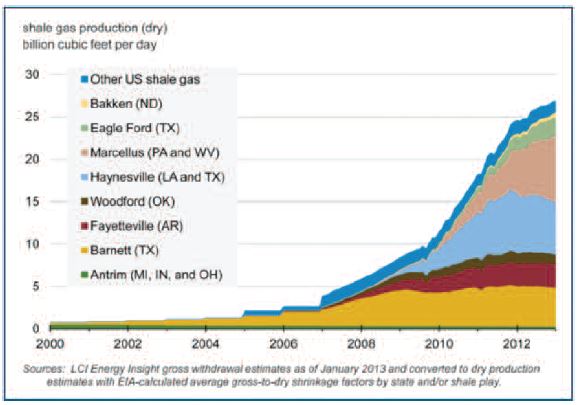

| My goal is to maintain the high quality of the Bulletin that the members have come to expect and to hopefully facilitate the exchange of ideas and thoughtful discussions on topics of interest to the society. I invite your contributions and feedback into making the Bulletin a publication that you enjoy reading and look forward to receiving each month. Look for some additional features during the next ten issues. These will include a return of the Geological Website of the Month which appeared in the 2008 – 2009 issues. The Internet has developed into an extensive resource and repository for a wide range of information including an abundance of geological, regulatory, and mapping information found on many governmental, educational, society, and industry websites. For many geologists, online resources have become indispensable tools for our jobs. Information that once required a visit to an academic library can now be retrieved in minutes on any computer with an Internet connection. Whether you are interested in geology career opportunities, current events, images of volcanoes, on-going research, or planetary science, you will find useful information. There are many informative and interesting websites dedicated to geological subjects. Enter the word “geology” into a search engine and more than 55 million results are found. Ten geological websites were featured in Volume 51. You can check the back issues to learn about websites for the United States Geological Survey, National Park Service, Geology.com, British Geological Survey, and many others. The revised feature will include a scorecard rating each website’s geological interest, visual appeal, and ease of use on a scale of zero to five rock hammers. Another new semi-regular feature will be titled Vintage Geology, an informal exploration of geologically-themed wines. Geologically-themed wines will have an earth science related name, term, or illustration on the label. This feature will include a brief discussion of the vineyard’s geological setting and its potential influence on the product.  The price of everything increases over time. Everyone knows that. Food costs rise, wages increase, goods cost more, and energy prices go up — except when they don’t. The price of everything increases over time. Everyone knows that. Food costs rise, wages increase, goods cost more, and energy prices go up — except when they don’t.The United States relies on a variety of energy sources to run the world’s largest economy. These include oil, coal, nuclear, hydroelectric, natural gas, and, increasingly, renewables. The prices of these energies are quantified daily on commodities markets in the United States and across the world. As of late-July 2013 the spot market price for a barrel of West Texas Intermediate crude oil was $107.84. Brent crude oil was $108.58 per barrel. The spot price of natural gas at the Henry Hub was $ 3.67 per million British Thermal Units (MMBTU). This natural gas price is up significantly from a recent low of $1.95 per MMBTU in April 2012. One British Thermal Unit, a somewhat archaic measure, is the amount of heat (energy) needed to raise one pound of water one degree Fahrenheit. Because oil and natural gas have similar uses as fuel and feedstock for chemical manufacture, one would think that their prices would be closely linked, rising together and falling together. But because these fuels have very different characteristics and different unit measures, how can one compare the price of oil with the price of natural gas? Comparison of Prices Logic would suggest that to compare prices, one must know the relative energy content of the various unit measures. After all, energy content is what users are paying for when buying hydrocarbons. While the energy content of crude oils will vary based on the region of production, in a rough measure one barrel of oil has approximately six times the energy content of one MMBTU of natural gas. This should make for simple arithmetic. A barrel of oil has six times the energy of one MMBTU of natural gas; therefore, a barrel of oil has the same energy content as six MMBTU of natural gas. This means that one barrel of oil should be six times the price of one MMBTU of natural gas. A quick check with a calculator reveals a disparity. Even after the recent price escalations, six times the price of one MMBTU of natural gas is still only about $22, much less than the current price of a barrel of oil. That means that in July 2013, the equivalent amount of oil energy is worth almost five times that of natural gas energy. What’s the deal? In a March 30, 2013 New York Times article Why One Gas is Cheap and the One Isn’t, Floyd Norris looked at the starkly different trends for the price of natural gas and the price of oil in the period from 1990 to 2012. Except for some spikes, the price of natural gas barely changed during those two decades and the price of oil increased more than five-fold. The biggest divergence in the pricing has occurred since 2008. During most of the period from 1990 to 2005, natural gas and oil were priced roughly the same on an energy equivalent basis. Then, between 2005 and 2012, the price of oil outpaced the price of natural gas until oil was more than eight times more expensive than natural gas in 2012. The price of natural gas has become decoupled from the price of crude oil. Why the Difference? Many years ago, while working for Texaco International Exploration, I was on a team that was involved in a major discovery of natural gas off the Northwest Shelf of Australia that became known as Gorgon. Thinking that the impressive flow rates of the discovery well test would please management, I was perplexed when the vice president had a pained look on his face and moaned, “Gas? !? Gas? What good is gas? That’s worthless. We can’t make money on that. I want something that you can carry in a bucket.” A large part of our economy is “hard wired” into using liquid hydrocarbons. The United States uses approximately 18.5 million barrels of crude oil per day, according to the U.S. Energy Information Administration. More than half of this amount is imported. The gathering, transportation, and distribution of these liquids involve sea-going tankers, pipelines, terminals, refineries, tank farms, railcar, tank trucks, and filling stations. The Institute for Energy Research reports that 70 percent of petroleum consumption in the United States is used for transportation. Cars, trucks, trains, aircraft, and ships have been the engines of the western economies for nearly 100 years. Workers commute, goods are moved to market, raw materials are delivered to manufacturers, and shoppers drive to the mall. This all involves liquid fuels based on oil.  Market Forces Market ForcesFloyd Norris in the New York Times says, ”the diverging prices reflect the fact that while oil and natural gas can substitute for each other in some uses, the markets for the two products are very different.” The infrastructure and market for crude oil are international in scope and relatively efficient. Oil moving around the globe in tankers can be diverted from one destination to another almost instantaneously in response to shifts in demand. A change in demand or supply in any region of the globe is likely to show up in prices everywhere. The natural gas market, on the other hand, is not a global one. There is a limited trade in liquefied natural gas, which can be transported in tankers, but most natural gas must move in pipelines over land. Natural gas prices have been rising in some parts of the world even as they have been falling in the United States. As most Americans know, the production of natural gas in the United States has been increasing in the last five to ten years. This increase is due largely to the development of unconventional production techniques, especial horizontal drilling and hydraulic fracturing of tight shale formations. Shale gas production in the United States has increased from less than one billion cubic feet (BCF) per day in 2001 to more than 25 BCF per day in 2012. The natural gas infrastructure is not as well developed as the liquid infrastructure. So, until the development of large-scale liquefaction operations that would make natural gas exports viable, United States production remains stranded in North America. The Future Most observers would say the future of natural gas in the United States is bright. The use of natural gas for electrical generation is growing and will continue to grow. Bigger and more numerous houses in the hot and humid southern parts of the nation will need to be air conditioned and smart phones will need to charged. However, the use of natural gas in transportation would be the big switch that makes the fuel competitive with oil in the marketplace.  Oilman billionaire T. Boone Pickens has become a strong advocate for the greater use of natural gas in the domestic energy mix by calling for the implementation of “The Pickens Plan.” One of the pillars of the Pickens Plan is “use America’s abundant natural gas to replace imported oil as a transportation fuel.” Here’s what Mr. Pickens said in an April 2013 article in Bloomberg Businessweek: “It starts with getting into the transportation sector. When I started the Pickens Plan in 2008, there were about 200,000 vehicles on natural gas in the world; now there’s about 16 million. That growth is coming from everywhere but the U.S.” “The best thing to do is focus on heavy-duty trucks and give them a tax credit. You don’t put natural gas in your corner gasoline station. You put natural gas in a truck stop. It’s a fuel that competes against diesel. There are about 8 million heavy-duty trucks in the U.S. If you convert them to natural gas, that boosts consumption by about 15 billion to 20 billion cubic feet a day.” Even though Mr. Pickens and others may have visions of a transportation system that uses vastly more natural gas or even greater increases in electricity generated by burning natural gas, our liquid hydrocarbon-based economy will be with us for a while longer. Until you can refuel your car from the natural gas line running to your house, you will still want a fuel that you can carry in a bucket. FOOTNOTE: The March 2012 article by Floyd Norris was fairly prescient in forecasting: “…futures traders think that the gap in prices will diminish but remain large. A year from now, oil prices are expected to be almost exactly where they are now, while natural gas prices are forecast to have risen more than 50 percent. If that happens, on an energy equivalent basis, crude oil will still be more than five times as expensive as natural gas.” Almost dead on. |

What's Old is New and Passing on Gas: The Decoupling of Energy Prices

What's Old is New and Passing on Gas: The Decoupling of Energy Prices